- >

- Blog >

- Private Health Insurance vs GeSY in Cyprus (2026): Which Do You Actually Need?

Private Health Insurance vs GeSY in Cyprus (2026): Which Do You Actually Need?

2.65%

GeSY employee rate

of gross salary (HIO, 2026)

€150

Annual co-pay cap

€75 for reduced groups

€50-400

Private premium

per adult, per month

€4,770

Max GeSY cost

per year (€180k income cap)

GeSY covers nearly every legal resident in Cyprus, yet thousands of expats still buy private health insurance every year. That is not a contradiction. The two products do different jobs. GeSY is the cheap public foundation. Private cover buys speed, choice and the things GeSY leaves out.

At DigiCare Insurance, a licensed Cyprus broker, we place both local and international plans. The setup we arrange most often is a hybrid: GeSY plus a private top-up. So the question worth answering is not which one wins. It is whether GeSY alone is enough for you, or whether you need more than it gives.

Is GeSY Enough, or Do You Need Private Health Insurance in Cyprus?

GeSY, the General Healthcare System, launched in June 2019 with outpatient services and expanded to inpatient hospital care from June 2020. And it works. After GeSY launched, out-of-pocket health spending in Cyprus fell from 45% in 2018 to 15% in 2022, and Cyprus ranked 29th in the 2024 Global Health Index (most recent available data, per the same source). So this is not a story about a broken public system. It is about matching your cover to how you actually live.

Who can rely on GeSY alone

GeSY on its own works well if you are:

- On a tight budget and broadly healthy

- Happy to start with a Personal Doctor (your assigned GP) and accept referrals

- Comfortable with some waiting for non-urgent specialist appointments

- Rarely travelling outside Cyprus for long stretches

- Without big dental or optical needs

If that sounds like you, GeSY probably covers everything you need, and you can stop worrying about private cover.

Who should add private cover

You should look harder at private health insurance if you:

- Want to book a specialist directly, this week, without a referral

- Travel often and need cover that follows you abroad

- Have a chronic condition that needs a specific consultant

- Are retired and value faster access and private rooms

For a wider view of expat options, see our guide to health insurance for expats in Cyprus.

What GeSY Covers in 2026, and the 6 Gaps Private Insurance Fills

Here is what GeSY includes:

- GP (Personal Doctor) consultations

- Specialist care, with a GP referral

- Hospital admissions in public hospitals and affiliated clinics

- Lab tests, X-rays, MRI and other diagnostics

- Prescription medicines from an approved list

- Accident and emergency care

- Basic preventive dental and physiotherapy

- Mental health support and maternity care

Now the gaps. These are the six things GeSY does not cover, and they are exactly what private plans fill:

Treatment abroad.

GeSY is Cyprus-only. Care outside Cyprus happens only through a rare HIO committee exception for serious cases.

Full dental beyond one annual check-up.

Extractions, fillings and most dental work are excluded.

Optical and glasses.

Eye tests and lenses are not covered.

Private rooms.

GeSY hospital stays are in shared wards.

Direct specialist access.

Without a referral, a specialist visit costs €25 instead of €6.

Original medicines.

GeSY supplies generics; branded originals you pay for yourself.

There is one mechanism behind most GeSY waiting complaints, and it is worth understanding. Personal Doctors have annual referral quotas, and they face fines if they go over. So they sometimes decline referrals for non-urgent issues. That pushes patients toward longer waits, or toward paying €25 to see a specialist directly. So when you read vague online grumbles about waiting times, this quota system is usually what is going on underneath.

For the full mechanics of registration and contributions, see how GeSY works in detail.

Who Gets GeSY Automatically? Eligibility by Residency Status

GeSY eligibility follows your residency status, not your nationality. This table shows where each group stands:

GeSY Eligibility by Residency Status

| Residency status | GeSY eligibility | Contributions | Private cover notes |

|---|---|---|---|

| Employed EU resident | Yes, once registered | 2.65% via payroll | Optional top-up for speed and gaps |

| Self-employed or Cyprus Ltd director | Yes, once registered | 4.00% (or 2.65% as Ltd employee) | Common to add private for choice |

| Non-EU national with work or residence permit | Yes, after permit + registration | 2.65% or 4.00% | Plan A needed first for the permit |

| EU retiree with S1 form | Yes, via S1 | None | Many add a private top-up |

| Newly arrived (pre-registration) | Not yet | None yet | Private cover legally required meanwhile |

A few practical points the official pages do not spell out clearly. The S1 form must be requested from your home-country insurer before you leave; allow several weeks, since timelines vary by country. It cannot be done retrospectively. For non-EU arrivals, the route runs through Plan A immigration medical insurance for the residence permit, then GeSY once you are registered and contributing.

Family members of foreign employees sometimes face registration delays. A short bridging private policy covers dependants during that wait. For EU residents working through the permit process, see our guide to Yellow Slip and Pink Slip health insurance, and retirees should read health insurance for retirees in Cyprus.

GeSY Cost vs Private Insurance Cost: The Real Numbers

This is where the two products look least alike. GeSY scales with your income and then caps out. Private is a fixed premium set by your age and the scope of cover.

GeSY vs Private Health Insurance: Cost Side by Side

| Feature | GeSY | Private insurance |

|---|---|---|

| Cost basis | % of income | Fixed premium |

| Employee rate | 2.65% of gross | n/a |

| Self-employed rate | 4.00% of income | n/a |

| Income cap | €180,000 | n/a |

| Maximum annual cost | ~€4,770 | ~€600 to €4,800 |

| Annual co-pay cap | €150 (€75 reduced) | Plan deductible varies |

| Specialist visit | €6 referred / €25 direct | Plan-dependent, often direct |

| Prescription | €1 per item (max €15 per prescription) | Often covered |

| Dental | 1 annual check-up | Full cover available |

| Treatment abroad | No | Yes on international plans |

GeSY figures per the Health Insurance Organisation (gesy.org.cy, 2026). Private premium ranges per Cyprus insurers and brokers.

A worked example helps. Take an employee on €40,000 gross. They pay €1,060 a year to GeSY (2.65%, per the financing page). Add the €150 co-pay maximum and their total GeSY exposure is about €1,210 a year. A mid-range local private plan for a healthy 35-year-old runs about €120 to €180 a month, or €1,440 to €2,160 a year, per Cyprus brokers. Run both together and you are looking at roughly €2,650 to €3,370 a year. The €4,770 maximum GeSY figure is corroborated by cyprus-consult.

One tax note: medical fund and health insurance contributions are deductible at up to 2% of gross income under Cyprus personal income tax rules (within the overall one-fifth cap on combined personal deductions, effective from 2024). Check the current rate with your accountant.

For real private premium data by insurer and age, see our international health insurance cost study.

For the full contribution breakdown by income type, see our GeSY guide.

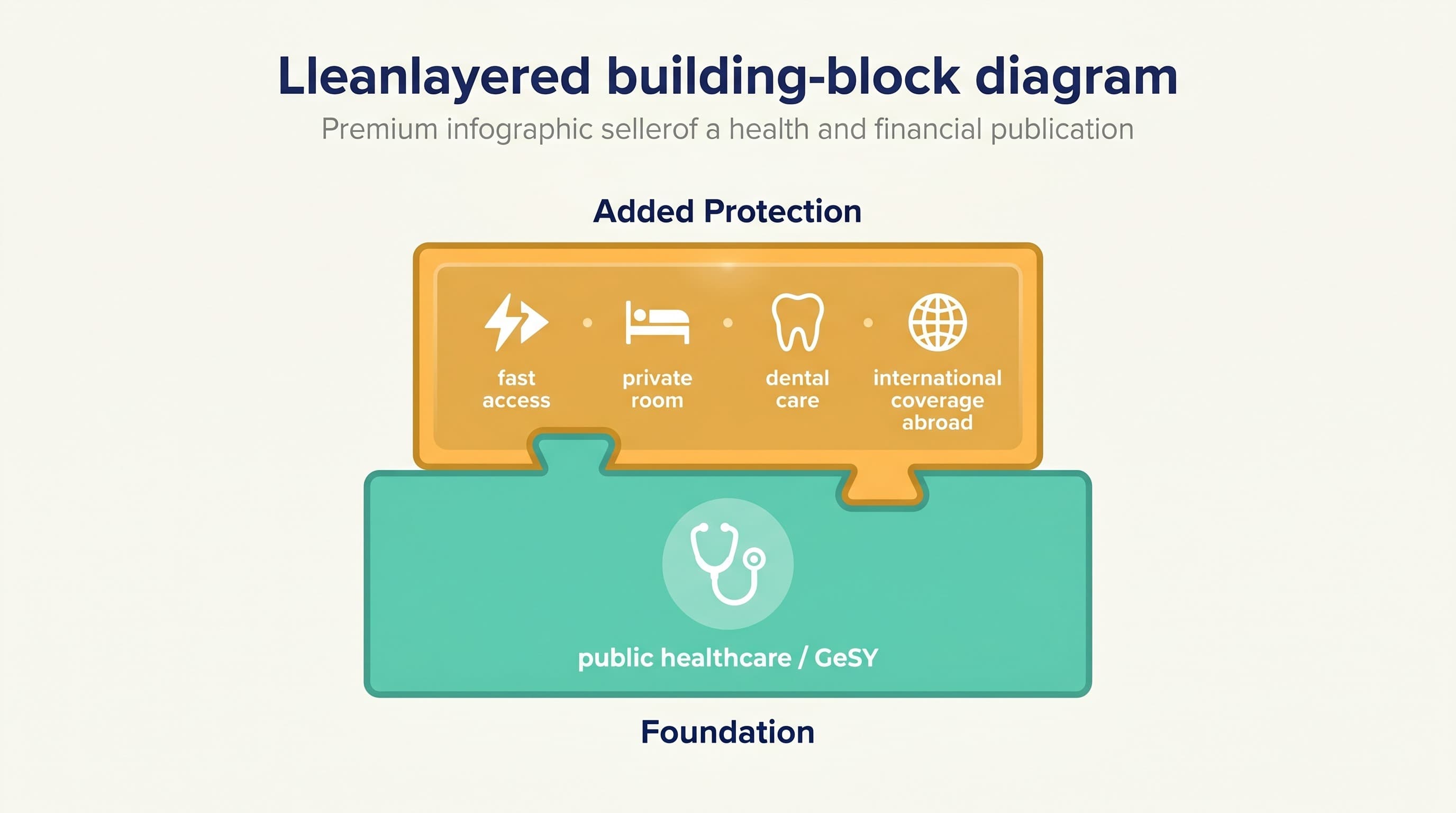

What Private Health Insurance Actually Gets You in Cyprus

Think about the experience, not the feature list. Each private benefit closes one of the GeSY gaps above. Where you really notice the difference is in how it feels to actually use the cover.

Direct access and speed

You book the cardiologist directly this week, instead of waiting for your Personal Doctor to free up a referral.

Full dental

The filling, the extraction, the crown, all covered, not just one yearly check-up.

Optical

Eye tests, glasses and lenses paid for, which GeSY does not touch.

Private room and private hospitals

A single room with your own bathroom after surgery, instead of a shared ward, with access to clinics that sit outside the GeSY network.

Treatment abroad and evacuation

You fly to Germany or the UK for a planned procedure, with the evacuation logistics handled, while GeSY would keep you in Cyprus.

Original medicines

The branded medicine your body tolerates, rather than the generic substitute.

The market backs this up. Cyprus has 32 domestic and 465 EU-registered insurers active. Many private clinics and specialists offer consultations in English, so a consultant can explain your diagnosis to you directly. And some private plans even reimburse your GeSY co-payments, per Cyprus brokers.

One caution. New private policies carry waiting periods, and they may exclude conditions you already have. We cover that in the next section. As a broker, we compare local plans like DCare Medical against international plans like Bupa Global, so you are not stuck inside one insurer's range. And because GeSY does not travel with you, frequent travellers should also read about travel insurance for Cyprus residents.

The Hybrid Strategy: Keeping GeSY and Adding Private Cover

This supplementary health insurance approach is the setup we arrange most often. The split is simple in practice. Lean on GeSY for everyday GP visits, repeat prescriptions and any big hospital event, because those are well covered at low cost. Save your private cover for the moments where speed and comfort matter: a same-week specialist, a private room after surgery, your dental and optical, or a procedure abroad.

Need bridging cover for your residence permit?

Get immigration insurance onlineThe S1 route for EU retirees

An S1 form gives EU pensioners full GeSY access without paying Cyprus contributions. Many retirees still add a private top-up, around €100 to €300 a month for a retiree per Cyprus brokers, for faster specialist access and private rooms. The S1 route is well documented for retirees settling in Cyprus. For more detail, see health insurance for retirees.

Why buying private young pays off

Age loading pushes premiums up sharply from 50 to 60 and beyond. Worse, any condition diagnosed before you apply can be excluded for good. So buying in your 30s and holding the policy beats starting at 55 with a page of exclusions attached. This is the single thing we wish more people did earlier.

Finally, some employers offer group health insurance that tops up GeSY for staff. If yours does, factor it in before buying your own. See group health insurance for businesses.

How to Choose: A Quick Decision Framework

Match yourself to one of these three tracks:

Stick with GeSY alone if:

- You are on a tight budget and broadly healthy

- You rarely leave Cyprus

- You are fine with referrals and some waiting

- Your dental and optical needs are minimal

Add supplementary private cover if:

- You want direct specialist access without referrals

- You travel regularly

- You want dental, optical or a private room

- You have a family with varied health needs

Make private your primary cover if:

- You are an EU retiree on S1 who wants comfort and speed

- You are in the pre-registration bridging window

- You need international-grade, multi-country cover, for example as a digital nomad

When you sit down to compare actual plans, check the inpatient versus outpatient scope, the hospital network, the pre-existing condition terms, the age limits and renewal guarantees, and whether treatment abroad and evacuation are included.

To pick a provider, compare the best health insurance companies in Cyprus, or read our concrete DCare Medical vs Bupa Global comparison. Digital nomads should also check the digital nomad visa health insurance requirements. When you are ready, compare private health insurance plans in Cyprus.

Insuring the whole household? Our family health insurance in Cyprus page shows real family premiums for couples and families of three or four, including how children are added as dependants.

Common Mistakes Expats Make with Health Cover in Cyprus

A handful of avoidable errors come up again and again in our office:

Treating Plan A as comprehensive cover.

Plan A immigration medical insurance is a standardised minimum policy for residence permits, not a real health plan.

Relying on EHIC or GHIC long-term.

The European Health Insurance Card covers emergencies during short visits only, not life as a resident.

Assuming GeSY covers treatment abroad.

It is Cyprus-only, and HIO committee exceptions for care abroad are rare.

Waiting until older or ill to buy private.

Age loading and permanent exclusions make late buyers pay far more for far less.

Treating it as strictly either/or.

Most expats who have done their homework run both, because the two products solve different problems.

More on the first pitfall in our Plan A guide. The EHIC limits for residents are documented by Expat Focus.

Looking for the GeSY portal login or how to register a Personal Doctor? That is covered in our GeSY Cyprus guide.

Frequently Asked Questions

Conclusion

For most expats the answer is the same one we give across the desk every week: keep GeSY as your affordable foundation, then add private health insurance in Cyprus for the gaps that matter to you. GeSY handles routine and major care cheaply. Private buys speed, direct specialist access, dental, optical, private rooms and treatment abroad.

Some people genuinely need only GeSY. Many need both. A few, like S1 retirees or digital nomads, lean mostly on private. Work out which track fits your residency status, budget, health and travel habits, then pick a plan to match.

Ready to compare your options?

Get a Free Health Insurance QuoteCompare GeSY top-ups and full private health plans for Cyprus.

Get a Free Quote