Professional Indemnity Insurance for Accountants & Auditors in Cyprus

DigiCare Insurance arranges ICPAC-compliant professional indemnity cover for accountants, auditors and audit firms across Cyprus. We have placed business insurance for over 15 years, and we match your cover to the €200,000 minimum ICPAC sets per claim.

- Independent Cyprus insurance agency, 15+ years

- ICPAC minimum €200,000 per claim

- Same-day certificate for your renewal

What is professional indemnity insurance for accountants and auditors?

Professional indemnity insurance pays your legal liability when a client loses money because of your accounting or audit work. It covers the compensation you owe plus the cost of defending the claim. You may see it called three things: professional indemnity, professional liability, or errors and omissions cover. They mean the same policy.

For accountants and auditors, the risk is real money lost on real work. A missed figure in a set of accounts, wrong tax advice, or a late filing can cost a client thousands. If they blame your firm, they can sue. This policy stands behind your professional judgment so one mistake doesn't put your practice at risk.

There's one more reason this cover matters in Cyprus: you have to hold it. The next section explains exactly what ICPAC requires.

See if your practice needs coverIs PI insurance mandatory for accountants and auditors in Cyprus?

Yes. Professional indemnity insurance is mandatory for accountants and auditors in Cyprus. It is required under the ICPAC Members' Rulebook, Article 7(2), as an ongoing condition of holding a practising certificate. No cover, no certificate. It's that direct.

The current minimum is €200,000 per claim. ICPAC raised this figure from the old €85,000 basis by a Council resolution dated 25 November 2015, and it took effect in 2016. The Council can revise the limit, so confirm the current minimum with ICPAC before you renew.

I get asked this every renewal season, so let me clear up one myth. One competitor guide online states that accountants in Cyprus are not required to carry PI cover. That is wrong, and it's out of date. The ICPAC Rulebook is the authority here, and it is clear: members in practice must hold the cover.

Audit firms have their own line. Rulebook Article 7(2)(a) requires every audit firm to make arrangements so it can meet damages arising from negligence in its work. So whether you practise as a sole accountant or run an audit firm, the obligation reaches you.

A quick note on the figures: €200,000 is a coverage limit, not a price. It is the amount the policy pays per claim, not what you pay for the policy. We cover what it costs next.

Get ICPAC-compliant coverHow much does accountant & auditor PI insurance cost in Cyprus?

Accountant and auditor PI cover in Cyprus typically runs from about €300 to €2,500 or more per year. A sole practitioner on the €200,000 minimum sits at the low end. A mid-size audit firm with high fee income, or one doing insolvency work, sits at the top and beyond.

Here is what shapes the premium in practice.

| Practice profile | Indicative annual premium | Typical limit |

|---|---|---|

| Sole practitioner | ~€300 to €700 | €200,000 (ICPAC minimum) |

| Small accounting firm | ~€700 to €1,500 | €200,000 to €500,000 |

| Mid-size audit firm | ~€1,500 to €2,500+ | €500,000+ |

These ranges are indicative. Your final premium depends on the points below.

Annual fee income and turnover

The cover limit you choose, starting at the €200,000 ICPAC minimum

Scope of work, since insolvency and liquidation work raises the premium

Territorial scope, if you serve clients outside Cyprus

Your claims history

The deductible you accept

You can buy more than the €200,000 minimum, and many firms do once turnover grows. Across the wider Cyprus market, professional indemnity premiums for all professions run from about €500 up to €25,000 for larger companies. Accountant cover sits at the lower, more predictable end of that scale.

We don't quote a single hard price on a web page, because no honest agency can. The number turns on your fee income, limit and scope. Tell us those three things and we'll come back with a real figure.

Get my exact premiumWhat does accountant PI insurance cover?

Two lists tell you most of what you need to know.

What it covers

Professional negligence in your audit or accounting work

Wrong tax advice that costs a client money

A misstatement in financial statements you prepared or signed off

A missed filing deadline that triggers a client penalty

Legal defence costs, even when the claim against you fails

What it doesn't cover

Fraud or dishonesty by you or your staff

Bodily injury and property damage, which fall under public liability insurance

Cyber events such as a data breach, which need cyber insurance

Management decisions about your own firm, which fall under directors and officers insurance

One point worth keeping straight: PI is not public liability. PI answers for your professional work and advice. Public liability answers if a visitor trips in your office. They are separate policies and you may need both.

If your firm holds client bank details, tax data and financial records, cyber cover is the natural companion to PI. A data breach isn't a professional negligence claim, so PI won't respond to it. We can bundle the two.

Not sure what limit covers your work? Ask usReal claim scenarios for accountants and auditors

These are the kinds of disputes that bring an accountant to our door. They are illustrative, not a promise of how any single policy responds.

The missed misstatement

An auditor signs off accounts that overstate profit. The tax authorities later penalise the client. The client says the auditor should have caught it and sues for the penalty plus the extra tax. PI funds the defence and pays the settlement up to the limit.

The wrong tax advice

An accountant advises a client on VAT treatment. The advice is wrong, the client underpays, and the tax authorities add penalties and interest. The client claims the difference back from the accountant. PI responds to the negligence claim.

The disputed insolvency engagement

An accountant acts on a liquidation. Creditors argue the process cost them money and bring a claim against the practitioner. Insolvency work carries higher exposure, which is one reason ICPAC ties its minimum to this kind of engagement. PI covers defence and indemnity within the agreed scope.

In each case the pattern is the same: a mistake, a claim, then PI steps in with defence costs and compensation up to your limit.

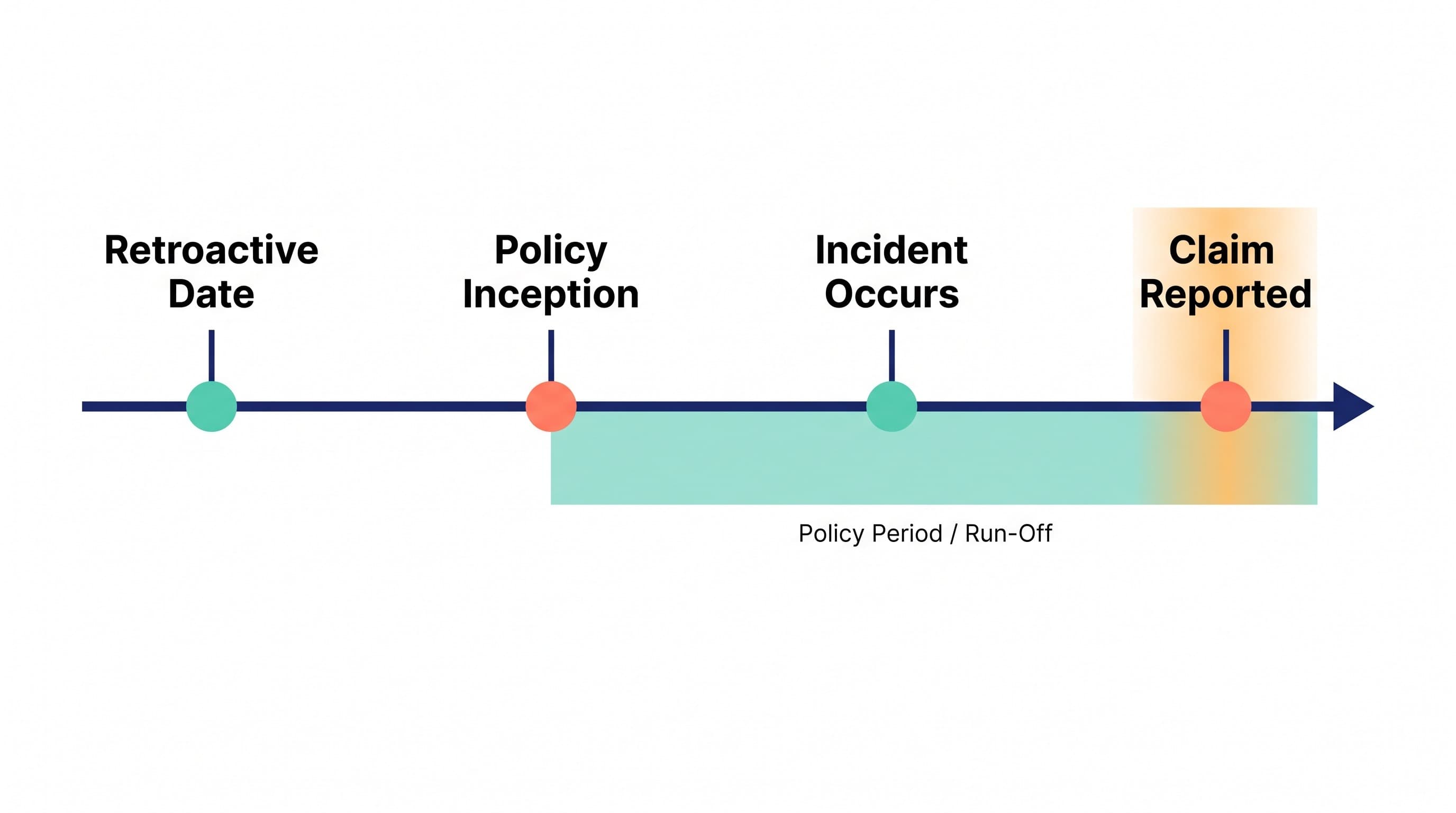

How accountant PI cover works: claims-made, retroactive date and run-off

PI is written on a claims-made basis. That means the policy that responds is the one in force when the claim is made against you, not the one in force when you did the work. So the practical rule is simple: keep your cover unbroken. A gap between policies can leave old work exposed.

Your policy carries a retroactive date. Work you did after that date is covered; work before it usually is not. When you've held continuous PI for years, that date sits far back and protects your whole career of accounting work. When you switch insurers, keeping the same retroactive date is what protects your past files.

Run-off cover handles retirement. When you close your practice or stop signing accounts, claims can still arrive years later, because a client may only spot a problem long after the work. Run-off cover keeps you protected through that tail. I'd flag it for any accountant winding down a practice.

On limits, you'll see a per-claim figure and sometimes a per-period total. The €200,000 ICPAC minimum is per claim. A sole practitioner and a busy audit firm rarely need the same limit, and we size it to your fee income and the work you actually do.

Talk to a PI specialist

Get accountant & auditor PI cover with DigiCare

DigiCare Insurance is an independent Cyprus insurance agency, and we've arranged business cover for over 15 years. We place ICPAC-compliant professional indemnity for sole accountants, accounting firms and audit firms, timed to your practising-certificate renewal so your cover never lapses.

We handle the parts that take time: the right limit for your fee income, how insolvency or international work changes things, and the paperwork ICPAC wants to see. Our team works in English, Greek and Russian. Tell us about your practice and we'll bring you the cover that fits.

Want the wider picture first? Read our guide to professional indemnity insurance in Cyprus. When you're ready, the quote takes a few minutes.

Get my free PI quoteFAQ

Accountant & auditor PI insurance questions

Renew your ICPAC cover before your practising certificate is due.

Don't let a lapse hold up your renewal. Send us your details and we'll confirm ICPAC-compliant cover, often the same day.